|

What is “The

Endowment?”

The endowment comprises many investment accounts. Income from some

of these can be spent for whatever the University wishes, but a

large number of these accounts are designated for specific purposes

(the Charles Howard Candler Professorships, the Henry Bowden Scholarships

and the Tenenbaum Lectureship are examples of such designated purposes,

and designated endowments exist in all the schools of the University).

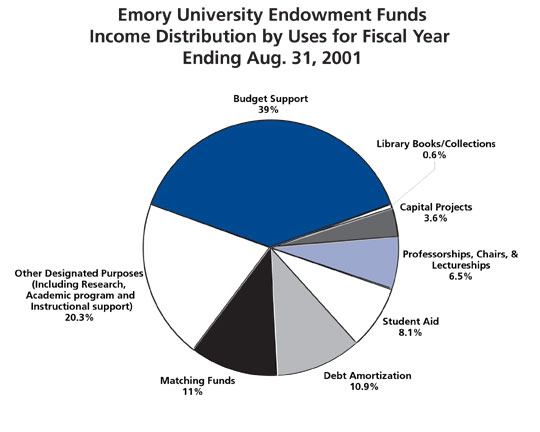

(See

pie chart) To use the income from designated endowments

for purposes other than those intended would constitute a breach

of trust to those who gave the money for those endowments.

On Aug. 31, 2001, the market value of Emory’s endowment stood

at $4.3 billion. Of that total, just over $2 billion (including

the $1.1 billion Emily and Ernest Woodruff Fund) was assigned to

the University in general, and about $2.3 billion was designated

for use by the schools, colleges and divisions. The general University

portion is further designated for uses shown in the pie chart. Using

a formula established by the Board of Trustees for determining how

much can be spent from the endowment, the board authorized $203

million in endowment spending for the last fiscal year.

How is “endowment

income” determined?

Until a few decades ago, universities were prohibited from spending

more than the dividends and interest on their endowments. Since

a change in the law, universities are permitted to use net appreciation

of the market value of their endowments, exercising, in the language

of the law, “ordinary business care and prudence under the

facts and circumstances prevailing at the time.” If an endowment’s

“book value” is $1 billion, but investment increases that

value to $1.5 billion, $500 million—or 33 percent of the “market

value”—could be spent.

In practice, however, that would be like someone’s inheriting

$5,000 and spending it all without regard to the future. What if

she loses her job next year? What if the house needs a new roof

in two years? What if she needs an operation? Wouldn’t it be

prudent to hang onto some of that inheritance and let it grow through

investment?

The Board of Trustees has the fiduciary responsibility of making

sure the University will be solvent a decade, a century, a millennium

from now. The board has therefore established a policy that the

administration may spend no more than 5 percent of the market value

of the endowment. Few universities, colleges or foundations spend

more than 5 percent of the value of their endowments.

For more than a decade the budgeted spending rate approved by the

board has been 4 percent, and for some years an additional 0.75

percent of unrestricted endowments has been applied to a capital

matching program, which has allowed the University to attract gifts

for projects like the Schwartz Center, Science 2000, the Goizueta

Business School and the Whitehead Research Building.

The spending rate, however, does not apply to all $4.3 billion

of the endowment; nearly $700 million is sequestered in the Woodruff

Health Sciences Center Fund, the income from which underwrites programs

in the health sciences. Restrictions on that endowment limit its

spending rate.

Similarly, the University’s cash management accounts are maintained

on the balance sheet as a part of the endowment but are not available

for spending at 4.75 percent. Only about three-fourths of the total

endowment can be spent at the 4.75 percent rate approved by the

trustees.

Why not spend a higher

percentage of the endowment?

The trustees’ spending policy has two purposes: First, it protects

the assets of the University for the long haul, ensuring that the

source of a significant portion of Emory’s income (20 percent

of the budget this year) will be there regardless of unforeseen

difficulties (e.g., the unlikely but plausible drying up of funding

for research, or a decline in enrollment and tuition, as happened

during World War II and the Korean War). Second, the limit on spending

prevents our committing too much too fast to programs in fat years,

and then not being able to continue supporting those programs in

lean years when the value of the endowment declines, as it has in

the last two years.

Retrospection—20/20 hindsight—is of course a great aid

in suggesting what spending rates could have been during

the bull market of the 1990s. Seeing what the market will do next

year or five years from now is a bit trickier. Even on the crest

of a wave, prudence dictates that we recognize the wave may crash,

the bubble may burst and the bull may turn into a bear.

But it is worth noting that even with a cautious policy, during

the unprecedented rise in the value of Coca-Cola stock during the

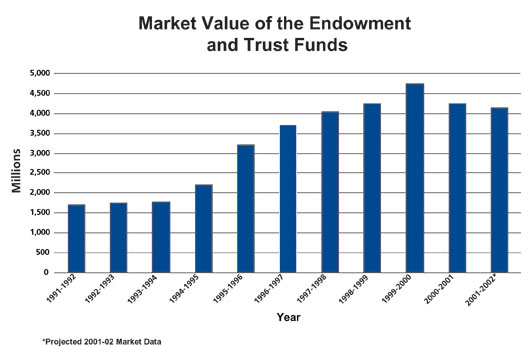

1980s and early 1990s, the University reaped great benefits (see

bar graphs). In several years during the 1990s, Emory’s

endowment grew by a greater percentage than any other university

endowment in the country. And from 1995 to 2000, spending from the

endowment grew commensurately. Emory converted much of that growth

in endowment spending to additional faculty lines, new buildings,

scholarships, research support, much-needed renovation of infrastructure

and new equipment. Had Emory not converted some of that extraordinary

appreciation of value into capital, we would have failed to realize,

or capture, some of that boon before the decline in market value

in 2000 and 2001.

Once the market turns

around, won’t Emory’s budget crunch be over?

It is worth noting that, as Emory’s endowment shrank in the

past 18 months, so did those of nearly every other university and

college in the country. Of the major university endowments, only

Yale’s grew last year. Of the endowments that shrank, Emory’s

did not lose the most in either dollars or percentage. The decline

in the S&P 500 (a benchmark for investment performance) for

calendar 2001 was 24.4 percent; the decline in Emory’s endowment

for that same period was 10 percent. These data suggest that the

endowment would have suffered some loss regardless of the asset

mix.

As is common in endowment management, Emory uses the average of

the past three years of market value to project spending for the

next year. The average of the past three years has not been good.

And it will be another three years before a market recovery has

any impact on the Educational and General Budget, assuming that

the recovery lasts.

Even despite the market downturn in 2000, however, income from

the endowment this year is greater than it was two years ago. In

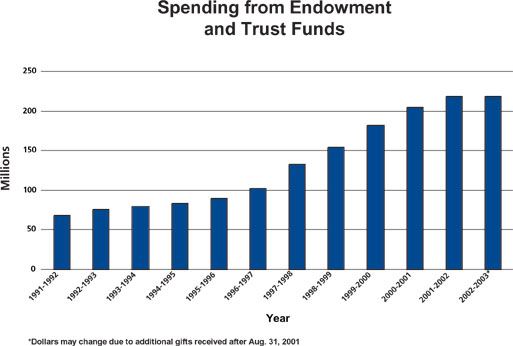

fiscal year 1997, when the endowment’s market value stood at

around $3.7 billion, spending from the endowment amounted to $102

million (of which $45 million went to the Educational and General

Budget). In the following years, as the endowment increased in value,

the spending rate remained the same but dollars spent from endowment

grew with the endowment’s market value, reaching $155 million

in 1999. Since then, the market has gone down, and at the end of

fiscal year 2001 the endowment was where it stood in 1998. Yet last

year endowment spending was more than twice what it was in 1997.

|